Public finance often looks technical from a distance. But sometimes, one policy shift captures a much larger story.

A simple way to understand the present moment is this: what happens when a government can no longer rely on a fiscal safety net, while at the same time its room to borrow is already becoming narrow?

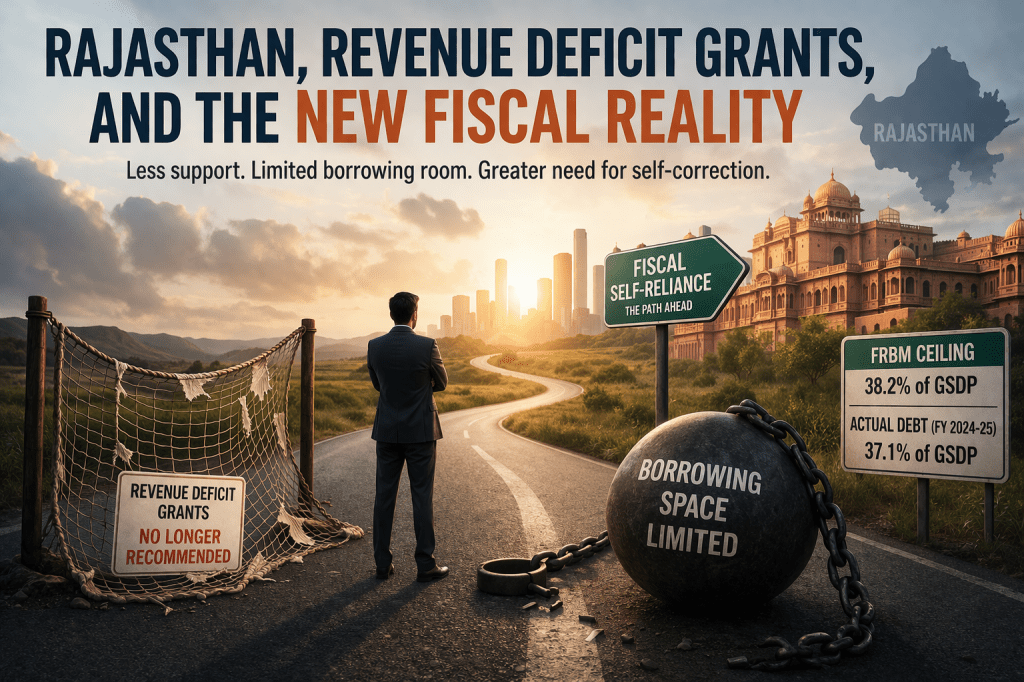

That is the broader question emerging from the changing treatment of Revenue Deficit Grants in the Finance Commission framework, especially in the context of Rajasthan.

The 15th Finance Commission: A Significant Revenue Deficit Cushion

Under the 15th Finance Commission, Rajasthan was recommended total grants-in-aid of ₹59,374 crore for the award period 2021–26. Out of this – ₹14,740 crore was recommended as Revenue Deficit Grant This was about 24.83% of the total grant-in-aid The full recommended amount was released.

This is an important point. Revenue Deficit Grant was not a minor component. It was a substantial part of the overall support package. In effect, it acted as a cushion for the State’s revenue-side imbalance.

The 16th Finance Commission: A Clear Policy Shift

For the 16th Finance Commission award period, the total grant-in-aid recommended to Rajasthan is stated to be ₹53,357.75 crore. But the more notable shift is this- No Revenue Deficit Grants have been recommended for the award period of 16th FC.

That is not merely a change in one line item. It suggests a deeper shift in fiscal philosophy.

The idea appears to be that States should increasingly manage their own revenue gaps through internal correction rather than through recurring external compensation.

Why This Shift Matters – Revenue Deficit Grants were meant to support States where revenue expenditure exceeded revenue receipts. When such support is available, it provides breathing room.

When that support is withdrawn, the expectation changes.The burden then shifts more directly toward: improving tax effort, increasing tax efficiency, rationalising expenditure, containing revenue spending, strengthening internal fiscal discipline

In other words, the framework moves from supporting the deficit to forcing correction of the deficit. Rajasthan’s fiscal capacity faces a double pressure. This transition becomes more significant when seen alongside Rajasthan’s debt position.As stated: the FRBM ceiling for debt is 38.2% of GSDP as per the Finance Accounts for FY 2024–25, the State’s actual debt is already accumulated at 37.1% of GSDP.

This creates a real double pressure on fiscal capacity. On one side: Revenue Deficit Grant support is no longer available. On the other side: remaining borrowing space is limited. That means the State cannot comfortably depend either on a revenue-gap grant cushion or on large additional debt space. Fiscal adjustment, therefore, has to come increasingly from within the system.

A larger change in fiscal federalism seen together- these developments indicate a broader transition in India’s fiscal federalism. Earlier approach supported States through revenue gap funding but emerging approach- expect States to correct deficits through their own fiscal management. This reflects a move away from compensating persistent imbalances and toward encouraging structural correction. Whether this shift will strengthen long-term fiscal resilience or deepen short-term stress is a separate debate. But the direction of policy is becoming clearer.

The Core Question Ahead

For Rajasthan, this is not just an abstract policy matter. It has direct implications for:- budget management, expenditure prioritisation, subsidy rationalisation, tax administration, fiscal sustainability.

The real question is no longer only how much support a State receives. The more important question is this:

How should a State respond when grant support reduces, borrowing headroom narrows, and fiscal adjustment has to come increasingly from within?

Reduced fiscal cushion. Limited borrowing room. Greater pressure for self-correction.

That is where the next phase of the public finance debate is heading.