The financial health of India’s cities is increasingly dependent on their ability to generate Own Source Revenue (OSR), which consists of taxes and non-tax revenues that Urban Local Governments (ULGs) have the legal authority to levy and collect. For the Urban Local Bodies (ULBs) of Rajasthan, navigating municipal finance presents a unique paradox. On one hand, the state boasts some of the most progressive legal and valuation frameworks in the country. On the other, it struggles with a highly depressed tax base heavily influenced by massive tax exemptions and broader demographic factors.

However, recent shifts in national funding policies—specifically the mandate of the 16th Finance Commission (FC-16)—make it clear that Rajasthan can no longer afford to ignore its OSR deficits, regardless of its urbanization levels.

The Urbanisation Hurdle: A Structural Disadvantage

At a macroeconomic level, a city’s ability to mobilize OSR is heavily tied to its degree of urbanization and economic base. Rajasthan is officially categorized as a “less urbanised large state,” meaning it has an urban population of less than 30% alongside a total population exceeding 35 million.

Data shows a direct, positive correlation between the level of urbanization and a municipality’s ability to generate its own revenues. For instance, metropolitan ULGs in more urbanized large states collect nearly 3 times the OSR of metros in smaller urbanized states, and a staggering 10 times that of metros in less urbanized states like Rajasthan . Consequently, Rajasthan’s ULBs inherently face a lower baseline revenue generation potential and structurally require more support for both operational and capital expenditures.

Self-Inflicted Wounds: The Cost of Massive Exemptions

While low urbanization naturally limits revenue buoyancy, Rajasthan severely restricts its own potential through highly generous tax policies. A major constraint on the state’s OSR mobilization is its policy of granting unusually large size-based exemptions for property taxes.

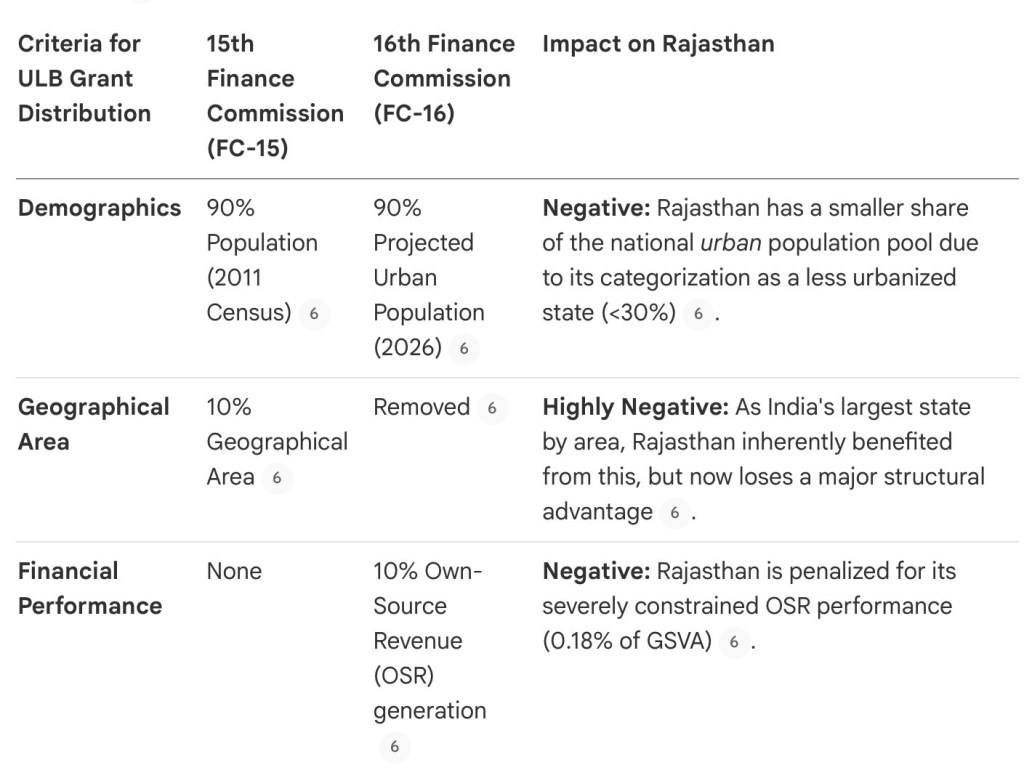

The state currently exempts all residential properties below 2,700 square feet and all commercial properties below 900 square feet. This creates a highly depressed tax base, severely limiting revenue potential. To put this in perspective, jurisdictions under the Mumbai Municipal Corporation Act only exempt residential properties below 500 square feet. Because of these massive exemptions, property tax contributes less than 10% of the total OSR for Rajasthan’s ULBs, and the state’s ULB OSR as a percentage of its non-primary Gross State Value Added (GSVA) sits at a mere 0.18%, lagging far behind leading states like Maharashtra (1.40%) or Gujarat (0.84%).

The 16th Finance Commission: A Wake-Up Call

The urgency for Rajasthan to overhaul its municipal finances stems directly from the 16th Finance Commission (FC-16), which has explicitly recognised urbanisation characteristics and made accelerating urban growth a central focus of its grants-in-aid. To incentivize speedier urbanisation, FC-16 shifted the macro-allocation of total local body grants between Rural Local Bodies (RLBs) and ULBs to a 60:40 ratio.

However, the methodological changes introduced by FC-16 structurally disadvantage Rajasthan.

Under the new FC-16 formula, Rajasthan’s inter se share for the ULB grant pool is fixed at 5.21%. The shift from a formula that rewarded geographical size to one that rewards urban population size and municipal revenue generation strongly indicates that Rajasthan has lost its previous structural advantages in securing urban grants.

Silver Linings: Progressive Frameworks to Build Upon

Despite these formidable challenges, Rajasthan presents a mixed picture because it has already implemented critical, politically difficult reforms that many other states lack :

- Capital Value (CV) Method for Property Tax: As of 2025, Rajasthan is one of only seven states in India to transition to the Capital Value method for levying property tax. This superior methodology ensures that property taxes are a buoyant source of revenue because it links the taxable value directly to state-notified guidance values or circle rates, reflecting actual market rates.

2. Legal Mandates for Water Cost Recovery: Rajasthan is one of only six states that have successfully implemented legal frameworks explicitly linking the setting of water tariffs to Operation and Maintenance (O&M) cost recovery. This protects the state from the severe under-pricing that plagues the 13 other states lacking such mandates.

Pathways Forward: How Rajasthan Can Augment OSR

To survive the fiscal shift brought by the 16th Finance Commission and ensure fiscal sustainability, Rajasthan must leverage its progressive frameworks and focus on specific levers to augment OSR:

- Roll Back Size-Based Exemptions: The most immediate fix is expanding the tax net by significantly lowering the massive exemption thresholds for residential and commercial properties, allowing the excellent CV valuation method to actually capture revenue.

- Enforce the Water Tariff Frameworks: Rajasthan must actively use its existing legal mechanisms to ensure water tariffs are formulaically linked to O&M costs, addressing the historical under-pricing of utility services.

- Monetize Municipal Assets: ULBs should create comprehensive, geo-tagged digital asset inventories of municipal lands and buildings, and establish robust legal frameworks to link rental income to market values.

- Leverage Land Value Capture (LVC): By integrating urban planning with finance, Rajasthan’s ULBs can tap into financial windfalls generated by public infrastructure projects through development charges and betterment levies.

Conclusion

Rajasthan cannot change its current urbanization levels overnight. However, it has total control over its municipal tax policies. By removing archaic property tax exemptions and fully utilizing its modern valuation and tariff frameworks, Rajasthan can overcome its structural disadvantages, improve its OSR buoyancy, and secure its rightful share of national urban development funding.

Leave a comment